A lot of people, especially those who live outside New York City, have only a vague notion what a co-op building is. Sure, they know it’s some sort of apartment but the details are often hazy at best. Yoreevo has you covered with everything you need to know before buying a co-op in NYC!

What is a co-op in New York City?

Is it worth buying a co-op in NYC?

What does a co-op’s maintenance fee cover?

What is an assessment?

What is the co-op board approval process?

How do I make an offer on a co-op?

Why are co-op buyers typically rejected?

Should I use a real estate agent to purchase a co-op?

What is a co-op in New York City?

Co-op is short for “cooperative.” When you buy a co-op apartment, you are actually buying shares in a corporation that owns the building. That might sound strange given a co-op listing advertises a specific apartment but technically, the buyer is purchasing shares. Just like you can buy 100 shares of Apple, you can buy 100 shares of 123 Main Street Corporation.

This compares to condos where you’re buying the specific unit or a house where you're obviously buying the entire house. In legal terms, both condos and houses are "real property." Co-ops, on the other hand, are "personal property" because you're buying shares, not real estate.

Don’t worry - if you buy a co-op, your fellow shareholders won’t have a key to your apartment!

Each owner is granted the right to occupy a specific apartment. This is called the “proprietary lease” for that apartment. Think of the proprietary lease and shares as a package deal - you get shares in the overall building plus the right to live in the apartment you "bought."

Unless you're specifically focused on condos, you'll certainly consider co-ops as they are about 75% of NYC apartment buildings.

Is it worth buying a co-op in NYC?

Most people in NYC are quick to hate on co-ops. Just search for "co-op horror stories" and you'll find plenty of entertaining anecdotes. But it’s important to note that every co-op sets its own rules. There are super laid back co-ops and others that deserve the criticism. So while there are general guidelines, make sure to ask questions about any building that you’re considering.

Disadvantages of a buying a co-op

There are a few clear negatives when it comes to co-ops such as:

Board Approval Process

When you're buying a co-op, prepare for a particularly invasive approval process. The board can ask for pretty much anything and you have one option - give it to them. There is no negotiating with a co-op board. We’ll address some common components of a board application later but for now, suffice it to say, co-op applications are more complex and take longer than a condo application.

Limited Subletting (Ability to Rent)

The ability to sublet (rent) a co-op is usually very limited. You need to follow the building’s sublet policy and get board approval for each sublet. Sublets can be outright forbidden or have no restrictions whatsoever. It depends on the building. Usually a co-op will require a shareholder to live in the unit for a period of time and/or restrict how often they can sublet their unit. The most common sublet policy is you need to live in the unit for 2 years and then you can sublet for 2 of the next 5 years.

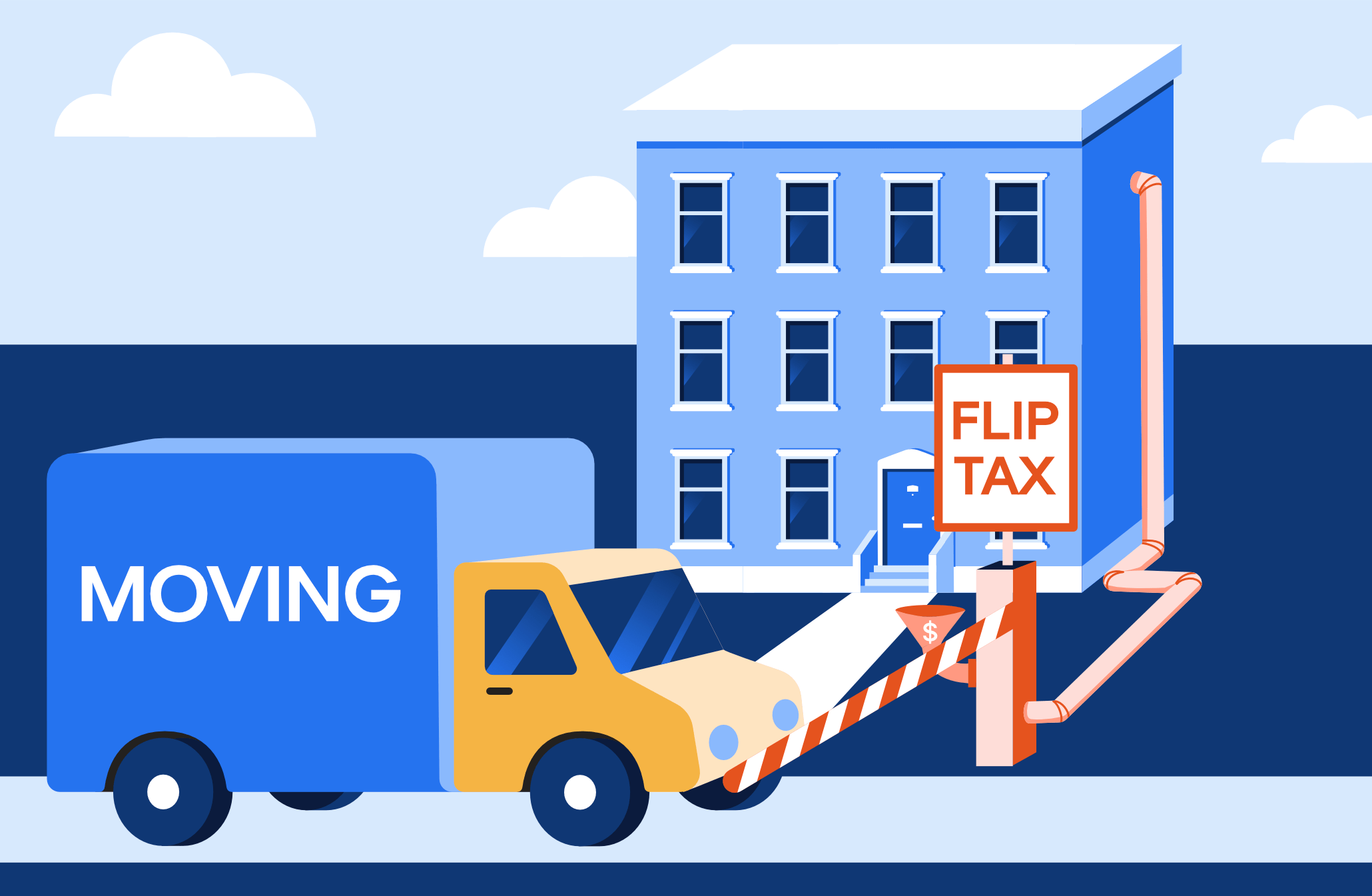

Flip Tax

A flip tax is a fee paid to the building when you sell. Just like the NYC and NYS transfer taxes, you can't avoid them. While flip taxes are sometimes found in condos, they're significantly more common in co-ops.

A flip tax isn’t necessarily a bad thing. If you plan on owning your apartment for a long time, it can be a positive because every time someone sells, their flip tax gets deposited into the building's bank account. All else equal, a building with a flip tax will have lower maintenance.

Yoreevo conducted a sample and found the most common flip tax, by far, was 2% of the sales price and most co-ops do have one.

Smaller Buyer Pool

Between their stringent financial requirements and foreign buyers restrictions, fewer buyers can qualify to purchase a co-op and fewer buyers means lower prices. This is more of a neutral factor - you buy for less and you sell for less - but it's still something to consider.

Advantages of buying a co-op

Co-ops Cost Less

Because of all the disadvantages above, co-ops cost less than condos. In very broad terms, we would say 20% to 30% less. This is without a doubt the #1 reason buyers choose co-ops over condos.

Lower Closing Costs

Closing costs are much lower on co-ops because you're buying personal property (shares and the proprietary lease) which avoids the mortgage recording tax. Co-ops also don’t require title insurance as the co-op knows exactly who owns each unit at any given time.

Security

After you get into a co-op, the application process works in your favor. Co-ops usually do background checks and condos do not so you can be pretty sure that your co-op neighbors are going to be squeaky clean.

Stability

Co-ops pretty much always have financial requirements that are stricter than a bank's. 20% down is required and buyers must have a debt to income ratio of below 30% or, more often, 25%.

These elevated financial requirements are part of the reason NYC did not see a housing crisis as bad as the rest of the country in 2008. Co-ops basically did not allow banks to make aggressive, problematic loans.

This is a significant positive as the last thing you want is a forced seller in your building. When someone needs to sell, especially in a bad market, it will usually be at a low price, dragging down prices for the entire building as future buyers use that transaction as a comp.

What does a co-op’s maintenance fee cover?

A co-op's maintenance fee combines property taxes and common charges into one monthly payment. In a condo, you receive a separate bill for each.

Maintenance is usually about 50% property taxes and 50% common charges. At the end of each year, co-op owners get a form from management detailing their share of the building's property taxes.

Common charges go to everything required to run the building - paying the doormen, cleaning the hallways, taking out the garbage, etc.

Maintenance can also cover planned capital improvements like painting the hallways or a new lobby.

What is an assessment?

All co-ops have a reserve fund. You can think of this as the building's checking account and it's used to pay day to day expenses. It also has some extra money for unexpected expenses but sometimes there isn't enough.

For example, if the roof starts leaking, it would have to be fixed immediately and roofs aren't cheap. If there is not enough money in the reserve fund, most co-ops will implement an "assessment." This is when an additional amount is added to each shareholder's maintenance bill. Usually this has a specific reason (like the roof) and a clear end date. Once the expense is paid, the assessment ends.

Assessments can also go towards discretionary projects like redoing the hallways.

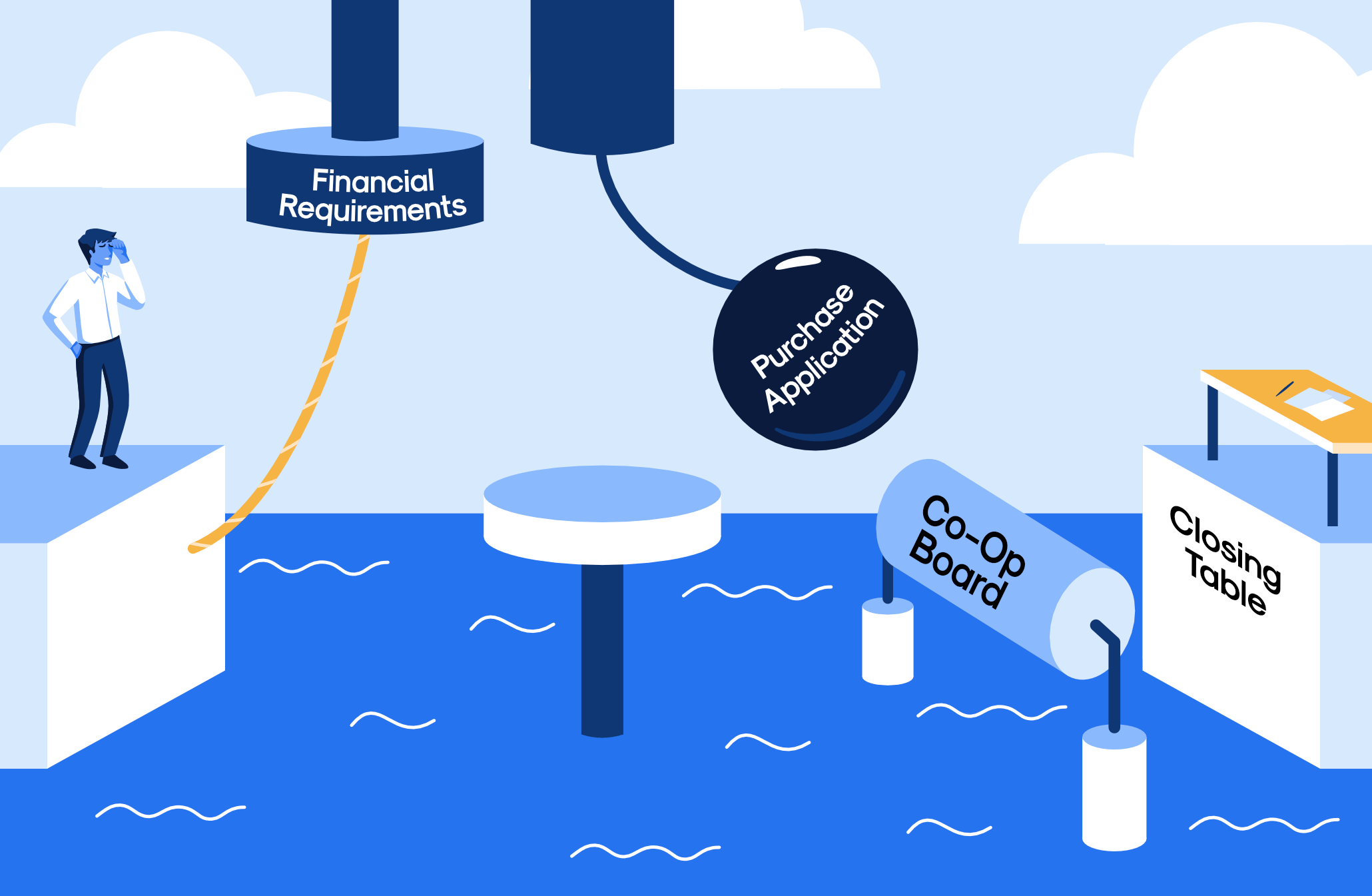

What is the co-op board approval process?

Getting approved by the co-op’s board of directors has three components -

Meet the co-op’s financial requirements

Virtually every co-op requires at least a 20% down payment. Some take down payments to the extreme and only allow cash purchases.

But even if you have plenty of cash, you still need an acceptable debt to income ratio ("DTI") to show the board that you can make your monthly payments.

Usually the monthly payment will simply be your mortgage plus maintenance but if you have student debt, a car loan, etc, those will also be included.

The target DTI for a co-op is usually 25% but sometimes you can go up to 30%. This is calculated as a percentage of your pre-tax income.

Boards also scrutinize post closing liquidity. This is simply how many months of payments you'll have in cash, stocks and any other liquid assets after you close. Anything that you shouldn't be selling (like retirement savings) or is hard to sell (like real estate) likely will not be considered. Most buildings want to see 12 or 24 months of post closing liquidity.

Co-ops have these strict financial requirements to avoid a forced sale. If someone stretches to purchase the most expensive apartment they can get and loses their job the day after closing, they're going to have to sell. That's a bad outcome for everyone - the buyer, other shareholders and the board.

Complete the co-op’s purchase application

For a detailed look at co-op applications, check out NYC Apartment Purchase Application Guide. Most co-op applications require:

- The completed purchase application with details of the transaction and the parties involved

- A copy of the signed sales contract

- A comprehensive financial statement with at least the most recent statement for each account listed

- 2+ personal reference letters

- 2+ professional reference letters

- A landlord reference letter

- An employment verification letter

- The last two years of full federal income tax returns

- Authorization to run a credit and background check

- Acknowledgement of the house rules

- Lead paint, bed bug and sprinkler disclosures

- If financing, the loan application, commitment letter and recognition agreements

- Checks for the application fee, move in deposit and other fees

After reviewing your application, the board of directors has three options - ask questions, invite you to an interview or reject the application. If your purchase is going to be rejected, it is usually at this stage.

Pass the co-op board interview

Co-op board interviews get a bad rap but aren't so bad. While you should be prepared for a full on, job-like interview, usually the board of directors just wants to welcome you to the building. They may ask you about yourself or your application but if there were any significant concerns, they likely would have been addressed before scheduling the interview. Board members don't want to waste their time so getting to the board interview is a very encouraging step.

How do I make an offer on a co-op?

Since the listing agent needs to have confidence you’ll satisfy the board’s financial requirements, making an offer on a co-op requires more information. On top of the actual offer and mortgage pre-approval, you'll also have to submit a REBNY financial statement. This provides a quick snapshot of your financials.

If the listing agent or seller has questions, you'll have to answer them. They need to be confident any offer they accept will be approved by the board.

We had a client get annoyed when a listing agent asked why they had such a high income but limited assets. We understood where both parties were coming from. The client found the question invasive but the listing agent knew the board was going to ask. Simply put, the co-op application process is not for everyone.

Keep in mind that any information requested at this stage will also be in the board application which the listing agent will review.

Why are co-op buyers typically rejected?

When a board rejects an applicant, they don’t have to (and typically don’t) give any reason whatsoever. The seller doesn't even get an explanation. While we don’t have data to back this up, our experience tells us the majority of rejections are for financial reasons.

For example, say a 30% DTI is required but a buyer with a 32% DTI makes a very strong offer. The seller might gamble and hope they get approved. Or maybe the buyer's DTI is below 30% on average but volatile year to year. The board might view that as too risky.

Boards also want to see good reference letters - both personal and professional. If something in a letter rubs the board the wrong way, they might hesitate to accept the application. An agent once told us she had a buyer rejected and the only thing she could point to was a personal reference letter that mentioned the buyer loved cooking a particularly pungent type of cuisine.

Sometimes the board will reject an applicant because they are getting too good of a deal. If the seller doesn’t care about money (and NYC has a few people like that!) and just wants to be done with the process, they might offer the apartment to their buddy or a neighbor for a low price. Since this affects the building's comps, the board will often reject these “below market value” transactions.

Should I use a real estate agent to purchase a co-op?

Many buyers think they can save a bundle if they forgo the use of a buyer’s real estate broker. It’s a fair assumption but the seller pays the same commission regardless. Most listing agreements are structured with the seller paying the listing broker 5% or 6% and then if the buyer has a broker, the commission will be split 50/50. Listing brokers love unrepresented buyers because they get paid twice as much.

For this reason, you should have a broker when buying. You'll have someone looking out for your best interests and negotiating on your behalf. Even better, you can use a buyer’s broker that provides commission rebates (like Yoreevo!). With a commission rebate, your broker gives part of their commission to you at closing. Yoreevo clients receive a commission rebate for two-thirds of the total commission, most commonly 2% of the purchase price which often covers a co-op's closing costs! Email us at info@yoreevo.com and we're happy to help!