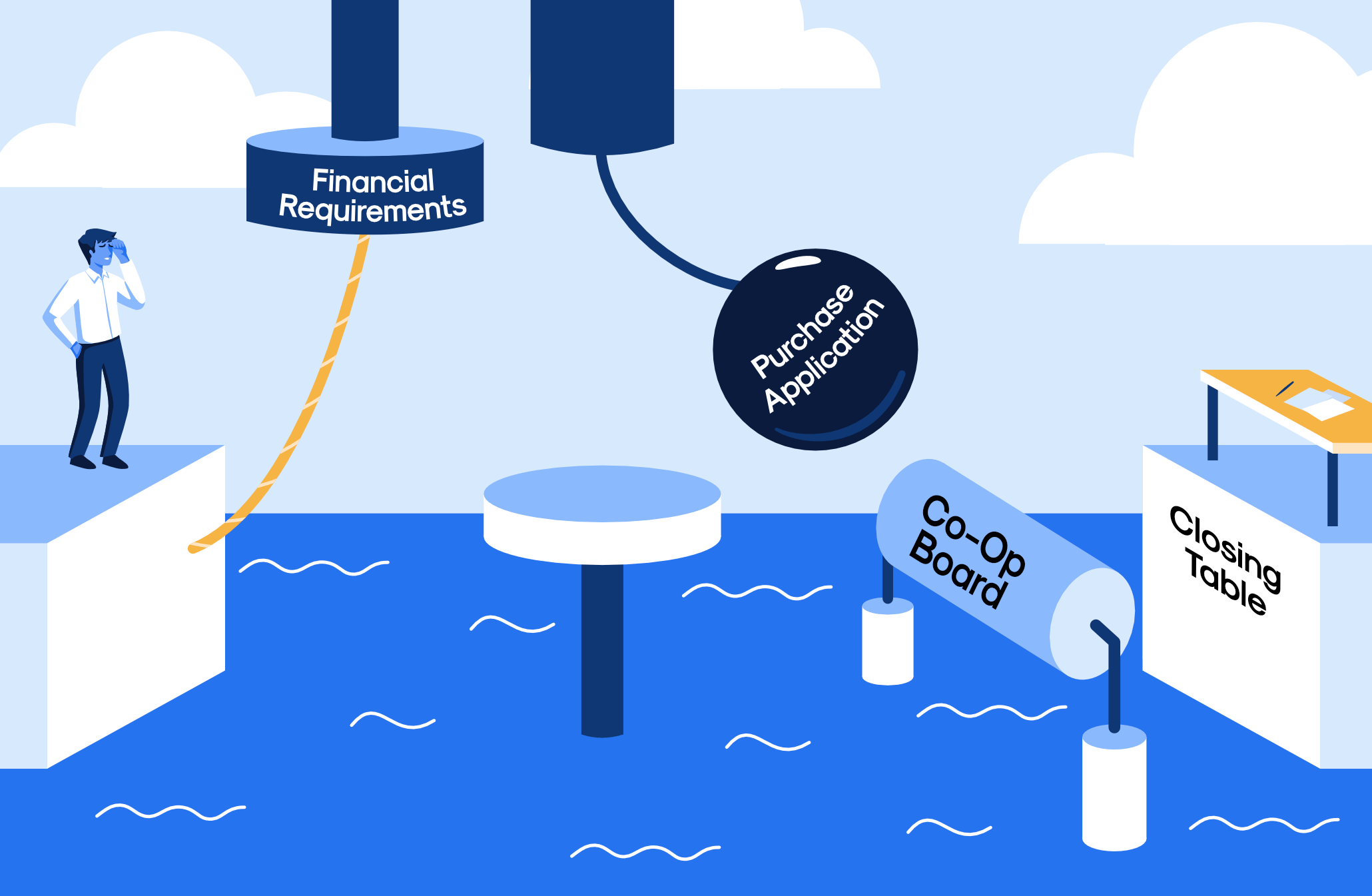

Whether you’re buying a co-op or a condo, you’re going to need to submit a board application (also called a purchase application). The list of requirements can seem daunting but not with this guide on your side! We’ve broken down each component so you know what to do and what not to do so you sail straight to closing!

Cover / Intro Letter

Most purchase applications do not require an intro letter but you should always include one. It’s your chance to introduce yourself and your application to the board. In addition to being a nice gesture, it also gives you the opportunity to explain anything quirky about your application.

It doesn’t need to be anything elaborate. Just a couple paragraphs with a quick background, why you like the apartment, building, neighborhood and thanking the board for reviewing your application. You can find a sample introduction letter here but make sure to make it your own. Boards see a lot of intro letters and if they think it's something generic that you copied, it can backfire. Add some quirky details about yourself to make sure it will stand out.

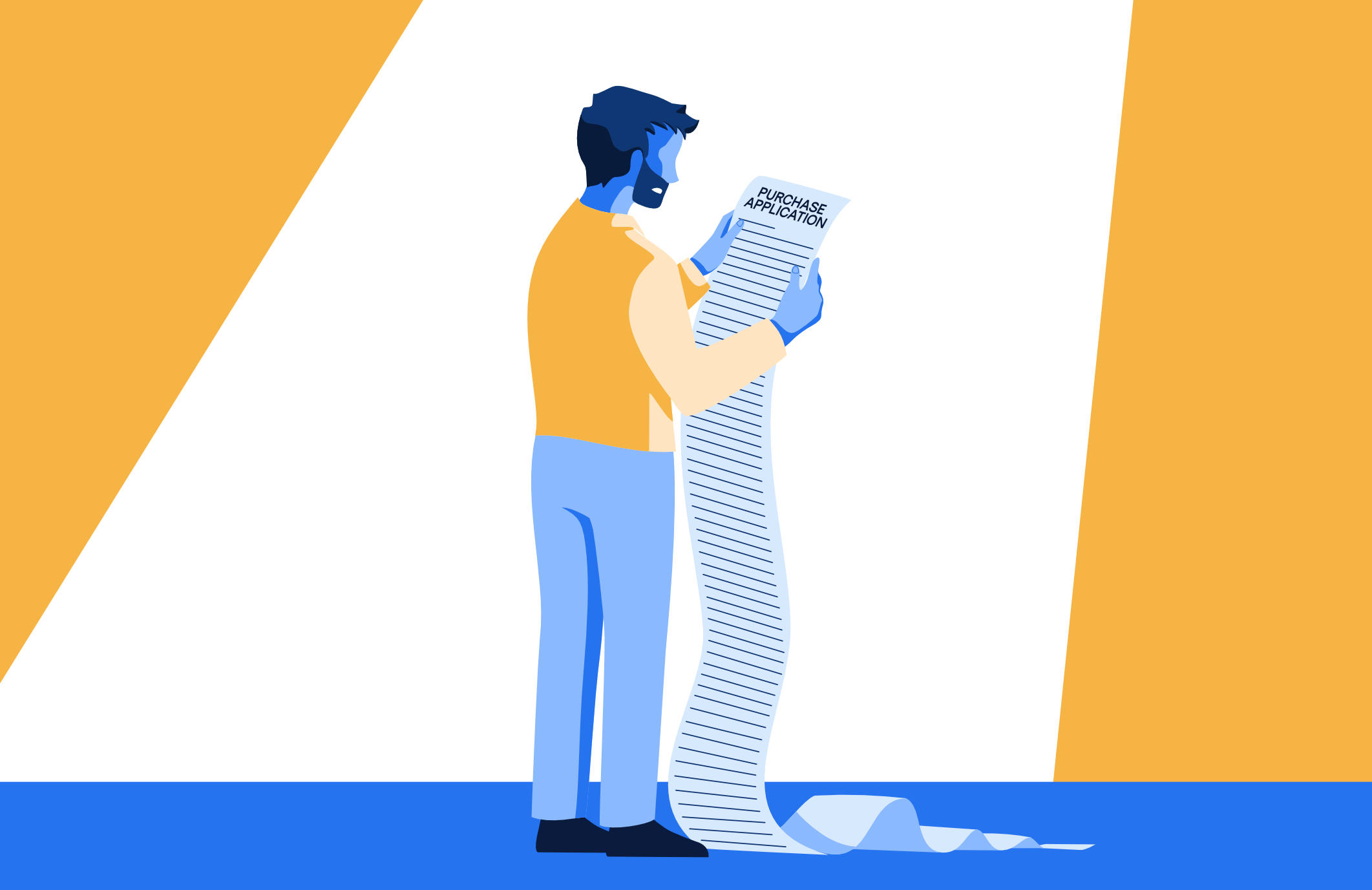

Purchase Application

Wait, isn’t this whole blog post about the purchase application? Yes but there’s also a piece that’s also called the purchase application. Every building is a little different but it’s basically a big form with everything the board could want to know about the deal - price, down payment, everyone’s contact information, your residence history, etc.

If a field doesn’t apply (like down payment in a cash deal), it’s best to put “N/A” so everything is filled in.

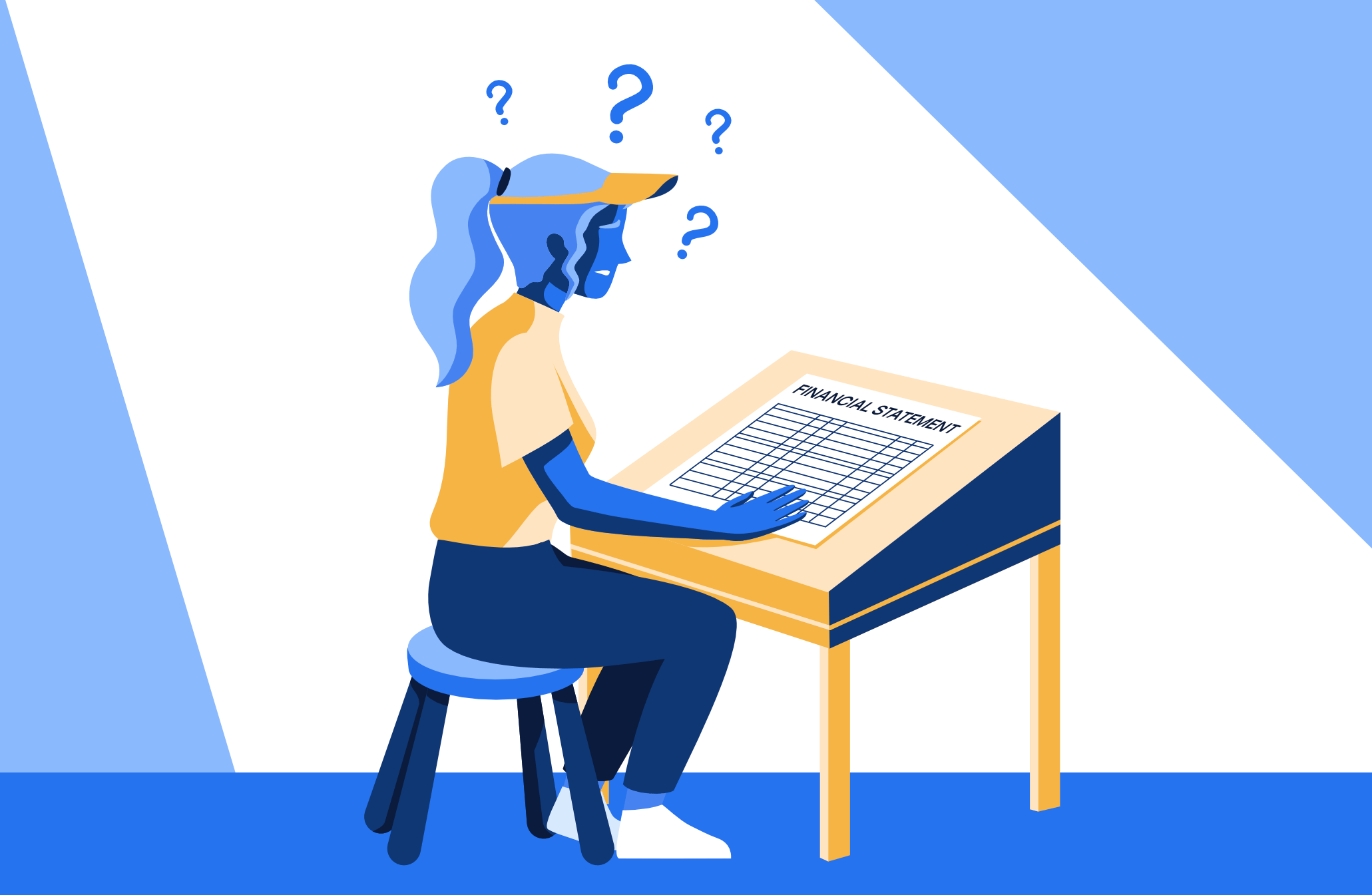

Financial Statement

When you made your offer, you likely submitted a REBNY financial statement. For the board application, you’re doing that again but all of the numbers are going to be backed up and exact. There will also be a schedule where you’ll list out your holdings in more detail.

Account Statements

Supplementing the Financial Statement will be your account statements. Make sure to confirm how many months of statement the board wants to see. Usually boards want to see up to the three most recent for each account.

Most applicants just have bank, brokerage and retirement accounts but anything you’re including in the Financial Statement needs to be backed up here.

A common complicating asset is other real estate because there is a lot to document - your ownership, its value, any mortgage and other carrying costs like property taxes. Usually a property tax bill (which shows property taxes and ownership), a mortgage statement and Zestimate will suffice. If the property is rented out, the lease should be provided

There are a lot of best practices here that will save you some headaches

- Circle or highlight account balances. This makes it easy for board members to follow along and pay attention to the right numbers.

- Circle or highlight the contract deposit. One of your assets will be the 10% deposit you put down when you signed the contract. Show the board the withdrawal on your account statement.

- Organize the statements from most to least liquid. Start with cash and end with retirement or real estate. When in doubt, look at the financial statement which is generally listed in decreasing liquidity.

- What do you do with life insurance? This is always tricky. If you have a regular term life policy, that does not go on the financial statement. The board only cares about another kind of life insurance policy called “whole life” which has a cash value and kind of a savings or retirement account.

- Remember everything needs to be backed up, including your income so make sure your salary matches your employment letter, your dividends match your tax return, your rental income ties to your lease, etc.

Tax Returns & W-2s

Make sure to sign your tax returns. Most people file their taxes electronically so never sign them but if you look near the bottom of the second page, you’ll find the signature line and boards will send your returns back if they’re not signed.

Also make sure your W-2s are originals from your employer, not the W-2 form that’s included with your tax return.

Reference Letters

You’re going to be asked for up to four kinds of reference letters - personal, professional, landlord and bank. Personal and professional reference letters should be unequivocally positive and say that you’re without a doubt the best applicant the board could ever ask for.

Listing agents and boards love to nitpick on the personal and professional reference letters but there are a few things you can do to help them sail through

- All letters should be property formatted with letterhead. If your professional references can use their company’s letterhead, fantastic, but you can always use your own.

- Personal reference letters can be about multiple applicants. Professional reference letters can only be about one applicant, obviously.

- Don’t ask family members - it sounds obvious but people do it!

- Get someone else to read them to make sure nothing can be misinterpreted as alarming.

Landlord and bank reference letters are more like factual statements in a standardized format. If you ask your landlord and bank for these, they should know what you’re looking for. A landlord reference letter basically says you’ve been a good tenant and the bank reference letter confirms your account details.

Looking for an example? Check out our full blog post dedicated to reference letters here.

Employment Letter & Pay Stubs

Every board purchase application will ask for an employment reference letter. It should have your position, hire date, salary and, if possible, any bonus.

Some employers are rigid about the information they’ll provide but having your previous bonus is helpful because it allows you to clearly document your income with one document. As an alternative, you can document your bonus with the relevant pay stub.

Fully Executed Contract

The easiest item on the list! Just ask your attorney for it and you’re done!

Pro tip: Every contract includes the lead paint disclosure and you can use it for the purchase application’s lead paint disclosure too.

Loan Commitment Letter

The commitment letter is your lender’s final deliverable before closing. It’s basically them saying, “We have all of Bob’s documents, did the appraisal and checked every box. We’re ready to issue the loan.”

The only wrinkle here is you want the final commitment letter. Lenders often jump the gun and issue one before the appraisal is ready which is not helpful or what you want.

Always make sure to send your commitment letter to your attorney before anyone else. They will make sure it’s the final version which is especially important if you have a financing contingency.

Once you have the final commitment letter, all you need to do is sign it.

Loan Application

This a standardized form with all of the information you submitted to your loan officer. All you need to do is ask them for a copy. There is sometimes a line for you to sign so take a look for that.

Aztech Recognition Agreements

Aztech recognition agreements are one of the most confusing parts of a co-op purchase application because they need to be originals. For more info on what recognition agreements are, check out our dedicated blog post here but the gist is it’s an agreement between your lender, the co-op and you to figure out what happens if you fall behind on your payments.

Later in your loan application, your bank will overnight three copies. You’ll sign them and submit them with the purchase application when the co-op can also sign them.

Even if you’re using an online application system, original recognition agreements must still be submitted. Condos do not require recognition agreements because they are real property, not shares.

Miscellaneous Forms

Every building’s purchase application has lots of miscellaneous forms to cover things like the house rules, their pet policy, lead paint and bed bugs disclosures, etc. They look like more work than they are - just sign and you’re done!

Checks and Fees

You’ll get nickel and dimed for a few fees when you submit your purchase application. Normally there is an application fee, credit check fee, move in fee and a few miscellaneous others and they usually need to be paid by bank checks.

A bank check is picked up in person and deducted from your account when issued so it’s guaranteed to go through.

The purchase application itself should specify how fees need to be paid. If anything is unclear, confirm with management first. If you can’t get a straight answer, go with a bank check. A bank check will always work, a personal check may not.