Title insurance is one of the most confusing buyer closing closings in NYC. It costs thousands of dollars and buyers often don't know what it is so what is title and why does it need to be insured?

What is Title?

In real estate, title is basically the right to own and use a piece of property. Title insurance makes sure you're actually buying that property, free and clear of any claims.

If that sounds strange, it is. Title problems and title insurance really only exist in the U.S.

In order to understand title insurance, it's helpful to run through some examples of what can go wrong with title -

- Fraud - The most extreme scenario is where the seller doesn’t actually own the property. Ever hear the saying about having a bridge in Brooklyn to sell you? If you bought the Brooklyn Bridge from a guy on the street but also managed to get title insurance, you’d be covered.

- Unknown Owners - This is most common when a property is inherited. One heir may sell only to have another pop up and claim they didn’t have the right to do so on their own. This could also happen during divorces or a number of other situations.

- Liens - A lien is basically an IOU that is attached to the property. Whoever owns the property, owes the money so you don’t want to unknowingly purchase a lien. Examples include unpaid property taxes and money owed to a contractor or “mechanic’s lien." The most common lien is actually just a regular mortgage but obviously that is paid off at closing.

What Does Title Insurance Do?

There are actually two two separate entities involved in getting title insurance - the title agency and the actual insurance company - and each has a different responsibility.

Title Agency - There are thousands of title agencies in the country. Think of them as the salesforce. They find transactions and present them to the insurance companies which actually issue the policies. As part of their job, they’ll run searches and make sure any potential issues are resolved prior to closing.

Most issues are discovered by the title agency prior to closing. Your contract will say the seller has to deliver “clear title” so if any blemishes are discovered, it's the seller's responsibility to fix them.

Title Insurance Company - After searching for and fixing any title defects, the file will be sent to a title insurance company which actually issues the policy. There are three large companies that dominate the industry - Fidelity National, First American and Stewart Title.

While you may deal with Sally’s Title Agency, Sally doesn’t actually issue the policy. One of those three companies will and if an issue arises after closing, you will file a claim with them. For example, if New York City informs you that guy on the street did not, in fact, own the Brooklyn Bridge, the insurance company would refund your money, not Sally.

There is one important distinction here - title insurance only insures the purchase price. If you buy an apartment for $800,000 and find an issue 20 years later when the apartment is worth $1,500,000, you would only have $800,000 of coverage. There are policies that pay out the appreciated value for an additional fee but almost all buyers purchase the standard policy.

Who Selects Your Title Insurance Company?

You pick your title insurance company. Your attorney usually steers the decision but ultimately, you’re paying so you get to pick.

Since the title agency is responsible for researching the title, they need to know what they’re doing. We’ve heard NYC attorneys complain about buyers who want to use their cousin’s title agency in Long Island. While they might do a great job in Long Island, not understanding the nuances of NYC real estate can cause problems.

That being said, as long as it’s a reputable, knowledgeable firm, you shouldn’t run into any objections.

How Much Does Title Insurance Cost In NYC?

Title insurance usually costs between 0.4% and 0.5% of the purchase price. The exact amount will depend on the purchase price and if you are getting a mortgage.

A lot of people think New York State sets pricing for title insurance. That’s not quite true. The Department of Financial Services approves rates that are set by each company and, more importantly, the Title Insurance Rate Service Association or TIRSA. All of the big title insurers are members of TIRSA so no matter where you go, prices won't change. TIRSA's rate manual was updated in October 2024 but the rates were unchanged.

The easiest way to determine your actual title bill is to simply ask for a quote. The quote will break down the total cost by line item so you can see exactly where the money is going.

For a general sense, check out this screenshot from TIRSA’s rate manual -

There are a couple steps required to calculate most title bills -

- Calculate the Owner’s Policy - Apply the rate on the left to each traunch up to the purchase price.

- Calculate the Lender’s Policy - Apply the rate on the right to each traunch up to the mortgage amount.

- Discount the Lender’s Policy - When you purchase the Owner’s Policy and Lender’s Policy together, the Lender’s Policy is reduced 70%.

We created a spreadsheet to estimate your title bill.

In addition to the policy itself, your bill will include smaller costs like a lien search and recording fees. These tend to be around $1,000 regardless of the purchase price.

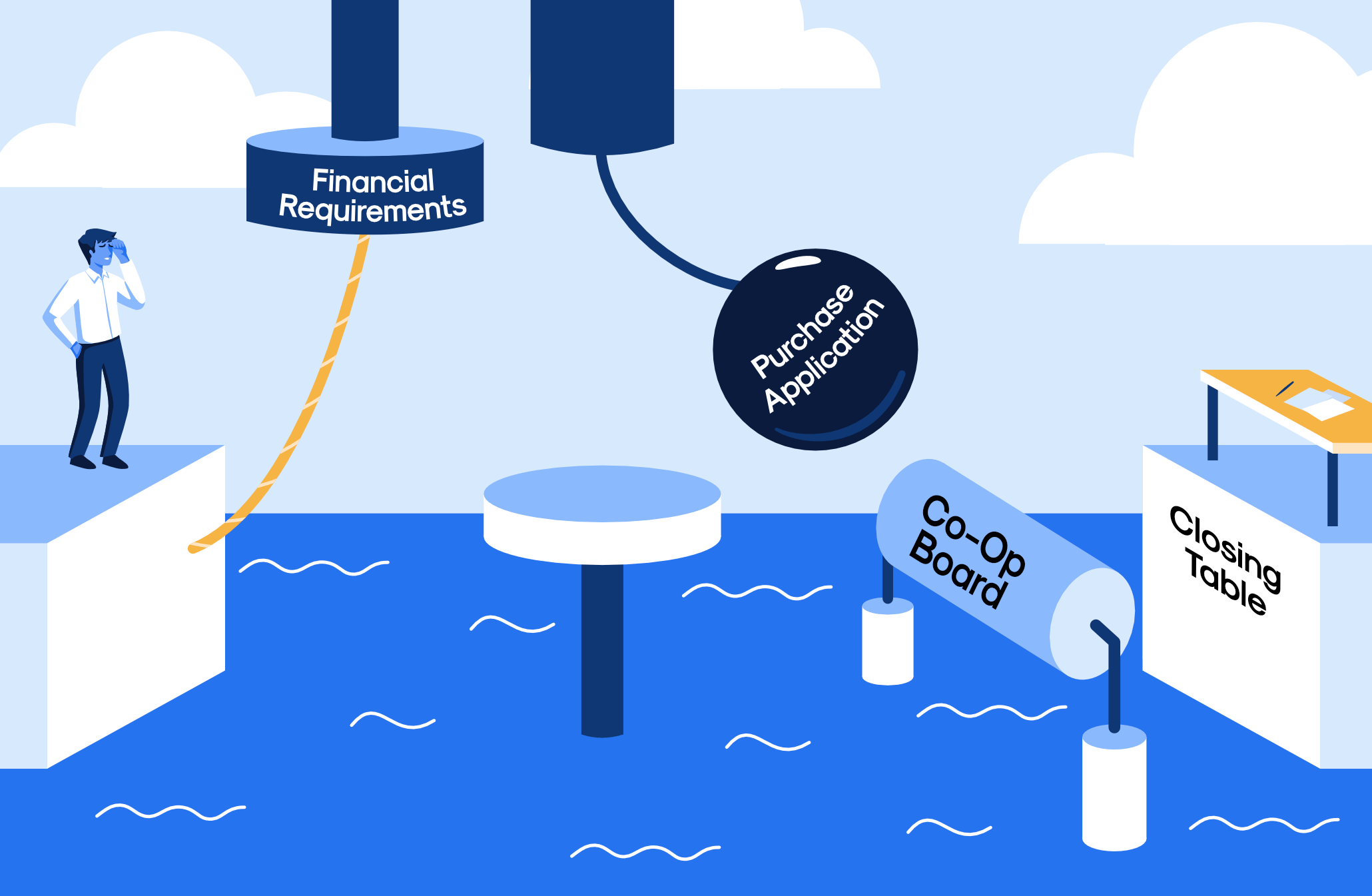

Do You Need Title Insurance in NYC?

Most NYC buyers are required to get title insurance for two reasons.

First, your lender will require a Lender’s Policy to cover the mortgage amount. Since the property is their collateral, they want to make sure they’re covered in case the property was sold fraudulently or some other issue arises.

Even if you’re paying cash, many attorneys won’t work on your transaction without title insurance. Your attorney’s job is to minimize risk and may feel waiving title insurance exposes you to too many issues.

One important distinction for NYC buyers - you do not need title insurance when buying a co-op. Only condo and house purchases require title insurance. When you buy a co-op, you’re actually buying shares in the building and the right to live in a specific apartment. You are not buying the apartment itself. This important distinction helps save on both title insurance and the mortgage recording tax.

As part of co-op due diligence, your attorney still do a lien search on the co-op itself to make sure there are no building-wide issues but this is significantly less expensive.

Is Title Insurance A Ripoff?

Just like any other type of insurance, title insurance can be very valuable but everything has a cost. Car insurance is valuable when you get into an accident but you wouldn’t pay $10,000 per year for it.

You'll be surprised to find out that less than 1% of what you pay for title insurance is actually paid out for claims.

The three big companies - Fidelity National, First American, and Stewart - are all public so we can see what percentage of revenue they expect to lose. This is called their “loss reserve” -

And remember, that's out of their share which is about 15% of what you pay. In other words, if you pay $1, less than $0.01 is actually getting paid out for claims. We’ll leave it to you to determine if title insurance is a ripoff!

How To Save On Title Insurance in NYC

With title insurance rates essentially fixed and policy rebates banned in New York State, there isn’t much room to save. That being said, Yoreevo does have two ideas.

- While policy rates are essentially fixed, there is flexibility in the ~$1,000 in fees you pay to research the property. Reach out to info@yoreevo.com for more information.

- It’s not a discount on the title insurance itself but Yoreevo can help cover the cost with NYC's commission rebate. Our average rebate is over $24,000 which can easily cover your policy and other closing costs!

Note: This post is meant for informational purposes only. Please consult a professional (attorney, title agency, accountant, etc) for any title insurance matters. Yoreevo is a real estate brokerage and does not provide title insurance.