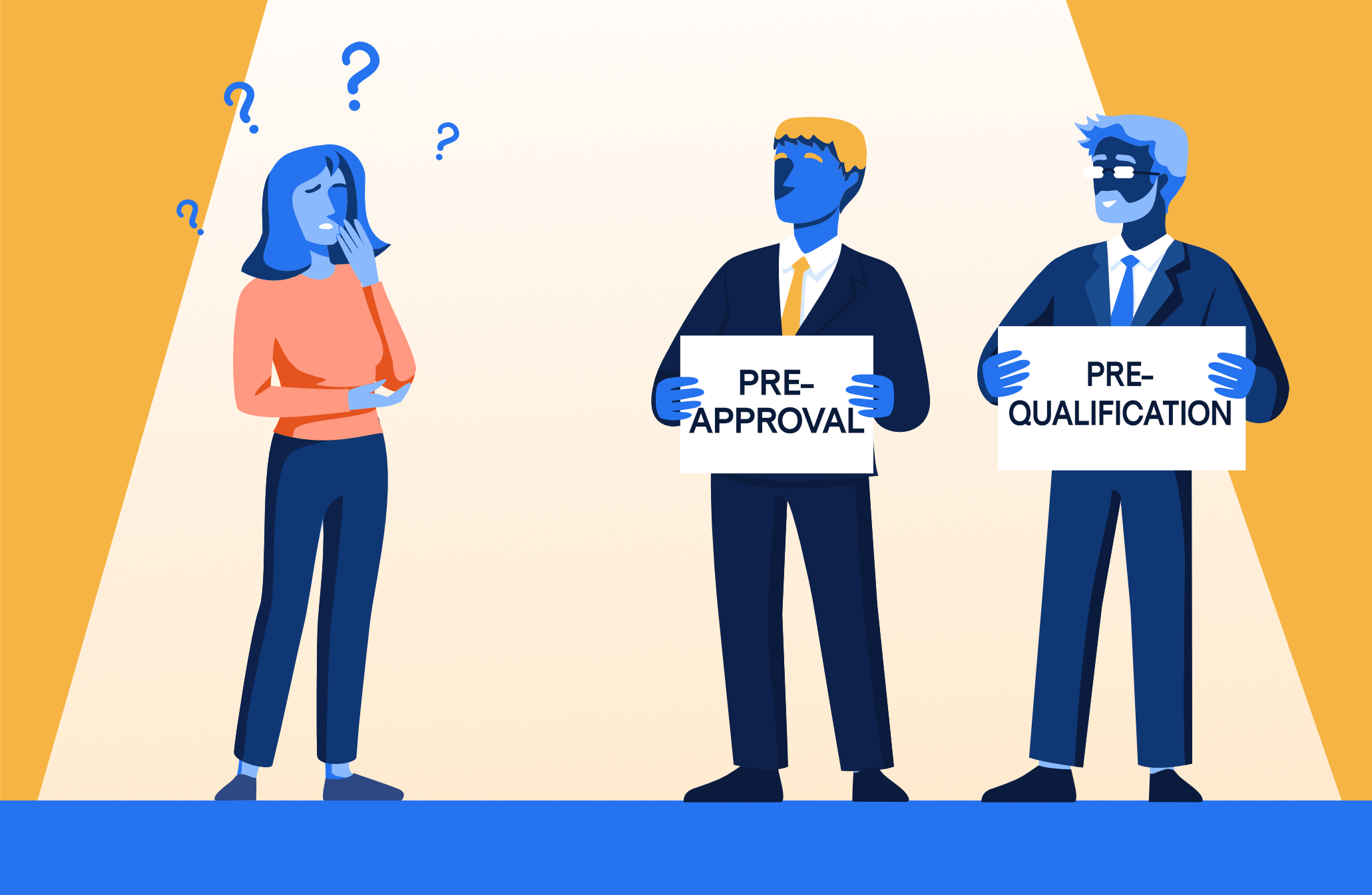

Pre-Approval vs. Pre-Qualification - The Difference

“Pre-approval” and “pre-qualification” are often thrown around interchangeably by buyers, brokers and even lenders but there's a big difference and it can impact how your offer is perceived by the seller.

Pre-Qualification - You can think of a pre-qualification as pre-approval-lite. You provide information to your lender and they give you a rough sense the loan you should be able to get.

It’s very inexact and not particularly reliable. If you provide incorrect or incomplete information, you could be pre-qualified for a loan you can’t actually get. For this reason, most sellers do not put much weight on a pre-qualification letter.

Pre-Approval - To upgrade to a pre-approval letter, your bank will order a credit check and do a more thorough review of your financials. You will also be asked how much of a down payment you plan to make. Because it requires more work, some lenders charge a fee but most are just happy to be your likely lender when you do buy.

Since the bank now has a good sense of your credit, financials and approximate transaction details, they will also be able to estimate your interest rate.

It's important to note that these definitions are not universal. While pre-approvals are generally more involved, that's not the case at every lender. If your lender did a credit check, verified your documents and issued you a letter with "pre-qualification" at the top, that's fine, just let your agent know so they can convey to the listing agent.

What is Required for a Pre-Approval?

In order to upgrade from a pre-qualification to a pre-approval, your lender or mortgage broker will require a number of additional documents. While every lender is different, the following are usually required -

- Completed loan application

- Federal tax returns including W-2s

- Photo identification

- Recent paystubs

- Bank statements

- Documents pertaining to current real estate holdings

- Information on any other outstanding debt

Should You Get a Pre-Approval or Pre-Qualification?

If you are serious about buying a home, you should get a pre-approval. While some sellers may not know or care about the difference, most do.

Yoreevo has had clients provide a pre-qualification and be asked to upgrade to a pre-approval and we don’t blame the sellers. The last thing anybody wants is to spend time and money going into contract only to find out that the buyer can’t actually purchase the property. Since getting a pre-approval letter takes some time, it's always best to take care of it early in your homebuying process. You don't want to be waiting for one with an offer deadline looming.

Is a Pre-Approval the Same as a Commitment Letter?

A commitment letter is the final deliverable from your bank before the actual check at the closing table. It basically says they’ve reviewed everything they need and will issue you the loan. It will also include some big picture contingencies like you can't lose your job before closing.

While a pre-approval does a good job getting under the hood of your financials, there are a few more boxes that need to be checked before you are issued a commitment letter.

Most importantly, your lender will order an appraisal. This is when a third party visits the property to assess its condition, take some measurements and estimate its value. Since the property is your lender’s collateral, they want to make sure you’re not overpaying. A low appraisal (lower than the contracted price) can be a problem as it limits the size of the loan your lender will make.

Assuming everything goes fine with the bank’s additional underwriting steps and the appraisal, you should have a commitment letter within a month of signing the contract.

Other Financing Considerations in NYC

If you are shopping in NYC, please keep in mind many apartment buildings have financial requirements that are more stringent than those of your lender.

This is particularly important in co-ops where buyers are expected to have a lower debt to income ratio, more post closing liquidity and down payment of at least 20%. You’ll want to make sure you talk to your real estate agent to make sure you’ll be approved by both your lender and the co-op board.

Don't have a real estate agent? No problem! Yoreevo is happy to help. Contact us and we'll run through your financials and have you on your way to getting a commission rebate!